Mortgage Rates Rise — Even After the Fed’s Rate Cut

If you’re wondering why mortgage rates went up even after the Federal Reserve cut interest rates, here’s what’s really happening behind the scenes in today’s real estate market.

Not all interest rates move in sync — and the Fed Funds Rate isn’t the same as a mortgage rate. The Fed’s rate mainly impacts short-term lending, while mortgage rates are driven by mortgage-backed securities (MBS) — long-term bonds that trade daily in financial markets.

Here’s the key takeaway:

So even though headlines said “Fed cuts rates,” the mortgage market reacted to the future outlook, not the current move.

What this means for homebuyers and sellers in the Central Texas housing market:

- Mortgage rates remain sensitive to economic expectations, not just the Fed’s decisions.

- Today’s rate movement isn’t a major spike, but it’s a reminder that timing and expert strategy matter.

- The best opportunities will come when new data signals real economic cooling — which could bring mortgage rates back down

If you’re thinking about buying or selling a home in Austin, Georgetown, Jarrell, or Round Rock, now’s the time to have a Realtor who understands how market shifts like this affect your next move.

Categories

Recent Posts

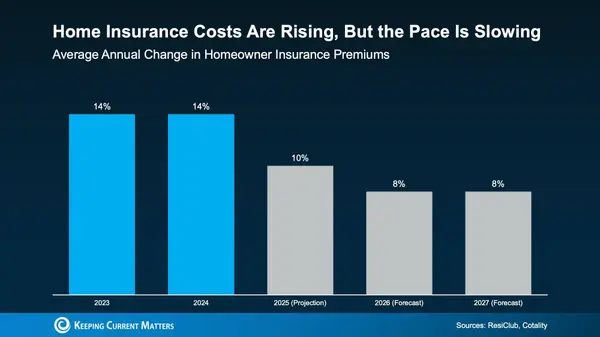

Home Insurance Costs Are Rising: What Today’s Buyers Need to Know Before Purchasing

Top 3 Reasons to Buy a Home Before the Spring Real Estate Market

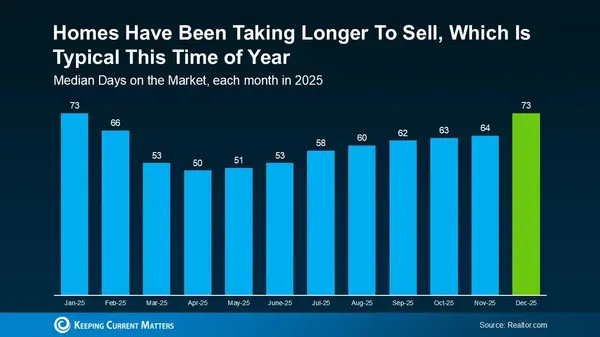

Don’t Overlook These Homes: Why “Days on Market” Can Signal Opportunity for Buyers

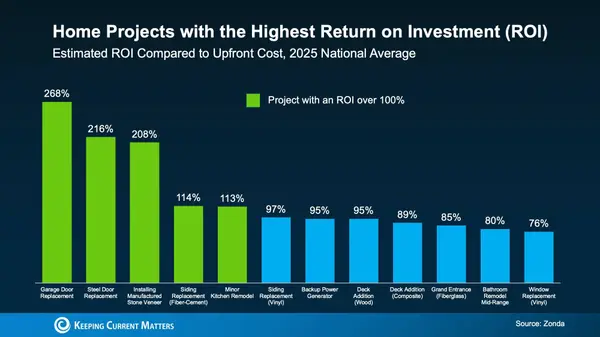

Home Updates That Actually Pay You Back When You Sell

The Credit Score Myth That’s Stopping Buyers From Owning a Home

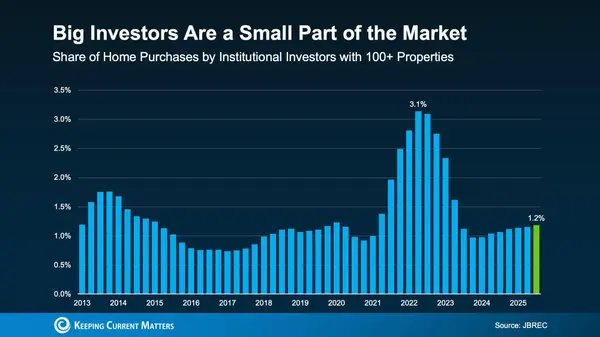

Are Big Investors Really Buying Up All the Homes? The Truth

What Realtor Credentials Really Mean for You as a Buyer or Seller

Buying a new construction home?

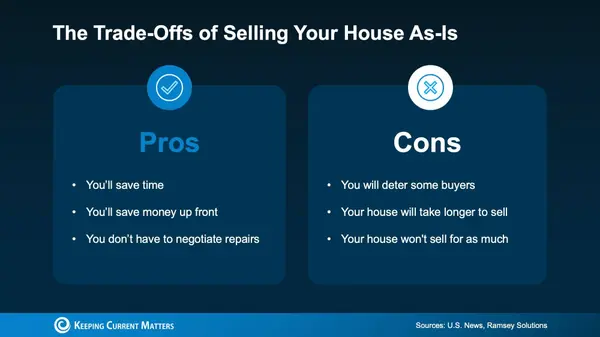

Thinking About Selling Your House As-Is in Today’s Real Estate Market? Read This First

Thinking About Buying a Home in the Next 12 Months? Start Here